Suppose that we are given a multivariate data set, and we want to

fit an Archimedean copula to it. How to proceed? It depends on

how much you are assuming known about the copula.

Parametrically

If you assume a

known family with finitely many unknown parameters, then we can

apply MLE in the usual way. This is the parametric situation.

Nonparamtrically

If you have no idea about the funactionl form of the generator,

then are in the nonparamtric situation. Genest and Rivest in

their 1993 paper have outlined a procedure to

cope with this scenario. We briefly present the idea below.

We shall work with only bivariate case. So our data set is

( X1 , Y1 ) , ( X2 , Y2 ) , ... , ( Xn , Yn ) .

Also we shall assume that Xi's are iid Unif(0,1)

and Yi's are also iid Unif(0,1). If you have any

other marginal, just estimate them and "fold them back". Te the

joint cdf of ( Xi , Yi ) be C(x,y) which is an

Archimedean copula with generator φ.

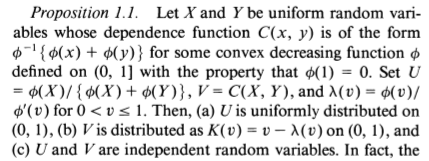

Genest and Rivest suggest a clever transformation of (X,Y)

to new variables (U,V) such that U has no

information about

φ (i.e., has no info about the copula)

while V has all the info about φ. Here is

Proposition 1.1 from their paper that gives this transformation:

Notice that φ can be recovered from λ as follows.

The nonparametric estimation procedure is as follows:

estimate C(x,y) by the empirical cdf Cn (x,y) and

define Vi = Cn ( Xi , Yi ).

Estimate the cdf K by the empirical cdf of Vi's.

Find λ from K.

Find φ from λ.

For the details (as well a proof of the proposition) see the

paper linked above.